Managing your finances can often feel overwhelming, especially when it comes to understanding personal finance ratios. However, these ratios can serve as your financial compass, steering you toward better budgeting, investing, and overall financial management. In this guide, we will explore the significance of various personal finance ratios, how to calculate them, and implement them in your daily financial decision-making. Let’s get started!

The Importance of Personal Finance Ratios

Personal finance ratios provide key insights into your financial health. They help you understand your spending habits, savings potential, and overall financial stability. By tracking these ratios, you can make informed decisions that align with your financial goals. Let’s delve into the primary ratios that everyone should know.

1. The Debt-to-Income Ratio

The debt-to-income ratio measures your monthly debt payments against your monthly income. A lower ratio is typically better as it indicates a healthier financial standing. Generally, financial experts recommend maintaining a debt-to-income ratio of 36% or less. That means no more than 36 cents of every dollar you earn should go toward debt repayment.

2. The Savings Ratio

Your savings ratio is the percentage of your income that you save. This ratio is crucial for building a safety net against unplanned expenses and ensuring a comfortable retirement. Financial planners often suggest striving to save at least 20% of your income. However, you can adjust this figure according to your personal finance ratios and specific goals.

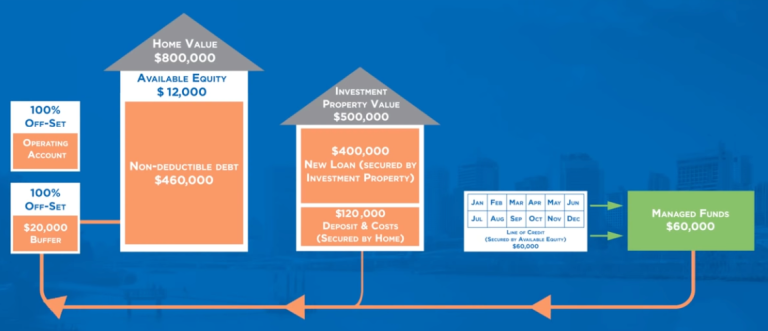

Visualizing Personal Finance Ratios

Understanding the intricate web of personal finance ratios becomes much simpler through visualization. Above is a savvy illustration showcasing various ratios in financial management. Use this image as a reference point whenever you feel lost in the world of finances.

3. The Liquidity Ratio

The liquidity ratio is crucial as it measures your ability to cover short-term obligations. To calculate this ratio, divide your liquid assets by your current liabilities. A liquidity ratio of 1 or higher indicates that you have sufficient resources to cover your short-term debts. This is vital during uncertain times, ensuring you remain financially stable when unexpected expenses arise.

Analyzing Your Personal Finance Ratios

Monitoring personal finance ratios regularly is essential for maintaining your financial health. Utilize budgeting apps or spreadsheets to track your ratios and see how they change over time. By keeping a careful eye on these figures, you’ll gain insights into your spending behavior and be equipped to make necessary adjustments.

4. The Financial Independence Ratio

This less commonly discussed ratio assesses how far along you are toward financial independence. Divide your total investments by your annual expenses to get this figure. A ratio higher than 25 indicates you are likely on the path to achieving financial independence — a goal that is becoming increasingly desirable in today’s society.

Practical Examples of Personal Finance Ratios

Let’s walk through some practical examples to solidify these concepts. Imagine you earn $5,000 a month. Your monthly debt payments total $1,500. Your debt-to-income ratio would then be 30% ($1,500 divided by $5,000). With a ratio under 36%, you’re doing well!

Next, if you’re saving $1,000 a month, your savings ratio would be 20% ($1,000 divided by $5,000). Again, you’re on a strong footing. Now, if you have liquid assets amounting to $10,000 and current liabilities of $5,000, your liquidity ratio would be 2.0, ensuring you can smoothly navigate any short-term financial hurdles.

5. The Return on Investment (ROI) Ratio

ROI helps gauge the profitability of your investments. By subtracting the cost of your investments from the total income generated and then dividing by the cost, you get the ROI percentage. A higher ROI suggests an effective investment strategy. Aim for an ROI above 10% for a healthy investment landscape.

Utilizing Personal Finance Ratios Effectively

To utilize personal finance ratios effectively, adopt a consistent review schedule. Quarterly evaluations can provide a clear picture of changes in your financial health and reveal trends over time. If you notice a troubling trend, take action right away. Adjust your spending habits, increase your savings, or consult with a financial advisor for professional guidance.

6. The Expense Ratio

This ratio reveals how much of your income goes towards monthly expenses. By dividing your total expenses by your total income, you can quantify your spending behavior. A ratio of less than 50% is often recommended, allowing for savings and discretionary spending. Being mindful of this ratio is crucial, as excessive spending can erode your savings over time.

Conclusion: Mastering Personal Finance Ratios

Understanding and managing personal finance ratios can lead to improved financial stability and peace of mind. Learning how to calculate and interpret these ratios is the first step toward mastering your finances. Regularly track your ratios, make adjustments as needed, and stay committed to your financial goals. By engaging with your personal finance ratios, you’re not just monitoring numbers — you’re paving the way to a financially secure and empowered future.

In summary, personal finance ratios act as critical tools in enhancing your financial literacy and decision-making. With this guide, you’re equipped to take control of your financial health and make informed choices that lead to lasting prosperity. Remember, knowledge is power, and financial knowledge can open doors to opportunities you never thought possible!