Securing a home loan is a significant financial decision that can impact your life for many years. However, for individuals with a low credit score, the journey to obtaining a home loan can be fraught with challenges. Home improvement loans, in particular, can help you increase the value of your property, making it essential to understand how your credit score influences your options. This article will delve into the nuances of acquiring a home loan with the lowest credit score for home improvement loans, providing you with insights and strategies to enhance your approval chances.

Your Credit Score and Home Improvement Loans: Understanding the Basics

Before we dive deeper, it’s essential to clarify what constitutes a low credit score and how it affects your eligibility for home improvement loans. Generally, a credit score below 580 is considered low. Credit scores this low can significantly hinder your ability to acquire loans, particularly favorable ones with low interest rates.

Why Lenders Care About Your Credit Score

When you apply for a home loan, lenders evaluate various factors to assess your creditworthiness. Your credit score is a critical component of this evaluation. It reflects your past credit behavior, indicating the likelihood of repayment. A low credit score often raises red flags for lenders, suggesting a higher risk of default. Thus, understanding how to navigate this challenge is crucial for anyone looking to secure a home improvement loan.

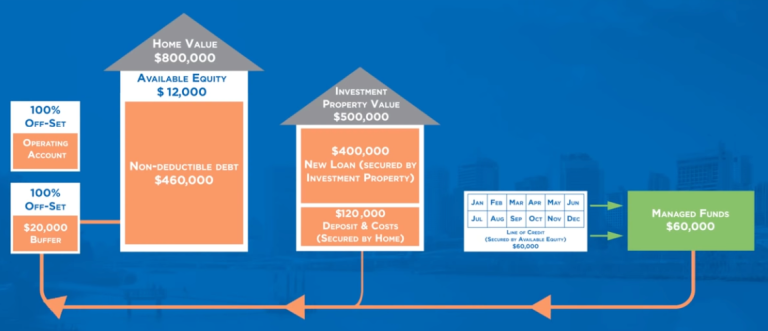

Image of Home Loan with Low Credit Score

This image illustrates the potential hurdles homeowners may encounter when seeking a loan with a low credit score.

Options Available for Low Credit Score Borrowers

Though obtaining a home loan with the lowest credit score for home improvement loans presents difficulties, various options can help you secure funding. Here are some avenues to explore:

FHA Loans: A Viable Solution

Federal Housing Administration (FHA) loans are designed to cater to individuals with lower credit scores. With these loans, you can qualify with a credit score as low as 580, provided you make a 3.5% down payment. FHA loans often come with competitive interest rates, making them an attractive option for those requiring loans for home improvements.

Consider a Co-Signer

Having a co-signer with a strong credit history can significantly bolster your application. This individual agrees to share responsibility for the loan, thereby enhancing your approval odds. However, it’s crucial to approach this option carefully; your co-signer’s credit could be affected if you default, potentially straining your relationship.

Explore Home Equity Loans

If you already own a home and have built up equity, you can consider home equity loans or lines of credit. These loans allow you to borrow against your home value, often providing more straightforward access to funding, even with a lower credit score. Keep in mind that these loans do put your property at risk, so careful consideration is warranted.

Improving Your Credit Score

If you are facing obstacles due to your credit score, there are steps you can take to improve it before applying for a home renovation loan. Engaging in these practices will not only enhance your approval chances but also lead to more favorable loan terms. Here are some strategies:

Pay Off Outstanding Debts

Your credit utilization ratio—the amount of credit used divided by the total available credit—plays a pivotal role in your credit score. Paying down debts, particularly those that are past due or near their limits, can lead to a significant increase in your score.

Check Your Credit Report

Regularly reviewing your credit report is essential. Errors or inconsistencies can drag down your score, and disputing inaccuracies can help you identify potential elements to rectify. You are entitled to one free credit report per year from each of the major reporting agencies. Utilize this resource to your advantage.

Establish a Payment History

Demonstrating a positive payment history is crucial for credit improvement. Ensure that all your bills, including those that may not report to credit agencies, are paid on time. This consistent behavior can enhance your credibility as a borrower and boost your score over time.

Long-Term Strategies for Future Loan Applications

While securing loans with a low credit score is achievable, establishing a long-term strategy for improving your credit can make future applications far more manageable. Here are some suggestions to keep in mind:

Increase Your Credit Limits

If you have a good relationship with your credit card issuer, consider requesting a credit limit increase. This can lower your overall credit utilization ratio, helping to improve your credit score. However, refrain from increasing your debt load, as doing so can counteract this strategy.

Utilize Secured Credit Cards

For those with very low credit scores, secured credit cards represent an excellent opportunity to rebuild credit. These cards require a cash deposit that serves as collateral, greatly reducing the lender’s risk. By using a secured card responsibly, you can gradually improve your credit score.

Diversify Your Credit Mix

Diverse credit types—such as installment loans, credit cards, and retail accounts—can positively affect your score. However, it is critical to manage this diversity wisely to avoid incurring excessive debt.

Seek Professional Help If Needed

If navigating credit repair feels overwhelming, consider consulting a credit counseling service. These professionals can provide invaluable guidance and develop a personalized plan for your financial situation. Opt for a reliable organization to avoid fraudulent services.

Conclusion: Making Home Improvements a Reality

Achieving your dream of financing home improvements with a low credit score is not only possible but also feasible with the right strategies in place. By understanding the implications of your credit score, exploring various loan options, and implementing corrective measures, you can enhance your chances of securing the funding you need. Remember, diligence and proactive management of your credit report can significantly improve your eligibility for home loans in the future. Through persistence and smart financial choices, homeownership dreams are well within reach.