In today’s fast-paced world, managing finances can be overwhelming, especially for young adults just stepping into their financial independence. Understanding key financial concepts, building solid habits, and setting achievable goals are crucial steps towards a successful financial future. In this article, we will delve into invaluable strategies that young adults can implement to gain control over their finances and thrive in a complex economic landscape.

Understanding Finances for Young Adults

Before diving into the specific strategies, it’s vital to grasp the foundational knowledge regarding finances for young adults. A solid grasp of personal finance basics—such as budgeting, saving, and investing—can pave the way to financial success. Young adults often face unique challenges, including student debt, high living costs, and the pressure to maintain a particular lifestyle. Being informed about these factors can help them navigate their finances more effectively.

Visualizing Success: Strategies for Managing Finances

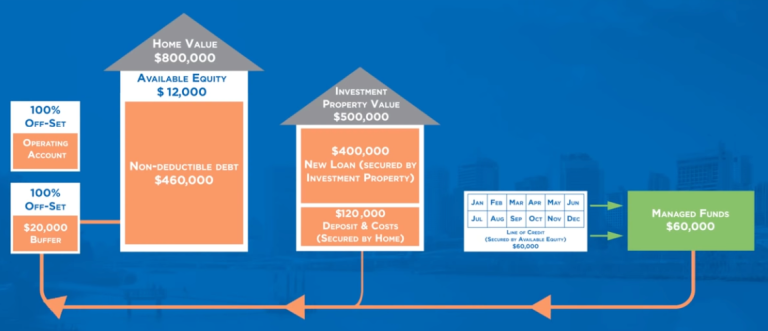

This image illustrates various pathways to achieving financial success for young adults.

Setting SMART Financial Goals

One of the primary steps in achieving financial stability is to set SMART (Specific, Measurable, Achievable, Relevant, Time-Bound) financial goals. When it comes to finances for young adults, clarity is essential. Rather than vague aspirations like “I want to save money,” a SMART goal would be “I will save $5,000 in the next year by setting aside $400 each month.” This specificity not only makes the goal seem more attainable but also provides a clear roadmap for how to get there.

Why are Financial Goals Important?

Financial goals are crucial as they give direction to your financial journey. They help young adults prioritize their spending and saving habits, ensuring that resources are allocated effectively. Furthermore, seeing progress toward these goals can provide motivation and a sense of accomplishment, encouraging individuals to stay committed and make informed financial decisions.

Budgeting: The Cornerstone of Finances for Young Adults

Budgeting is one of the most effective tools in managing finances for young adults. A well-defined budget allows individuals to track their income and expenses, making it easier to understand where money is going and identify areas for improvement.

Creating Your Budget

To create a budget, start by listing all sources of income, followed by fixed and variable expenses. Understanding all financial obligations is crucial in determining how much discretionary income is available. Several budgeting methods can be effective, such as the 50/30/20 rule, where 50% of income goes to needs, 30% to wants, and 20% to savings. Adapt the method to what works best, and regularly review it to adjust as necessary.

Establishing an Emergency Fund

Part of financial literacy includes understanding the importance of having an emergency fund. Life is unpredictable, and unexpected expenses, such as medical emergencies or car repairs, can occur anytime. Young adults should aim to save at least three to six months’ worth of living expenses to create a financial safety net. Setting up automatic transfers to a savings account can facilitate this process, ensuring that saving becomes a priority rather than an afterthought.

Building Your Emergency Fund: Tips and Tricks

When starting an emergency fund, it is often helpful to begin small. Setting aside a specific amount each month, even if it’s just $50, can eventually add up over time. As financial situations change, revisit and adjust the savings amount to ensure that the emergency fund remains adequate and prepared for unexpected events.

Understanding Debt Management and Credit

Finances for young adults frequently involve navigating the intricate world of debt and credit. In an era where student loans are common, understanding how to manage this debt responsibly is crucial. Prioritizing paying off high-interest debt first, such as credit cards, can save money over time and improve credit scores.

The Importance of Credit Scores

Your credit score can significantly impact your financial decisions, affecting loan approvals and interest rates. Young adults should monitor their credit regularly, ensuring that they manage debt responsibly—never exceeding 30% of their credit limit—and paying bills on time. Consider utilizing credit responsibly and aiming for a good credit score as it will benefit future financial endeavors like applying for mortgages or car loans.

Investing for the Future

Another essential aspect of finances for young adults is understanding the basics of investing. While saving is essential, investing allows money to work for you. By putting money into stocks, bonds, or mutual funds, young adults can build wealth over time, especially when considering inflation. Start by contributing to employer-sponsored retirement plans, such as a 401(k), to take advantage of employer matching and compound interest.

Beginning Your Investment Journey

Consider seeking guidance from financial advisors or utilizing investment platforms that offer educational resources. Diversifying your investment portfolio is also crucial, as spreading investments across different asset classes can help mitigate risks. The earlier young adults start investing, the greater their potential returns can be due to the power of compounding.

Continuous Financial Education

Finances for young adults isn’t a one-time lesson; it’s an ongoing journey. Continuous learning about financial products, market trends, and personal finance strategies is imperative. Books, podcasts, webinars, and articles (like this one!) are excellent resources to expand financial knowledge and stay updated on financial literacy.

Engaging with the Community

Interact with others who share similar financial goals through workshops or local meetups. Discussing financial experiences, challenges, and successes can lead to new insights and strategies that may prove beneficial. Surrounding oneself with a supportive community can also result in accountability which is instrumental in achieving financial success.

In Conclusion

Embarking on the journey to financial success requires proactive habits, disciplined budgeting, and continuous learning. By implementing these strategies, young adults can effectively manage their finances, set and achieve meaningful goals, and build a robust financial future. Remember, the sooner one begins managing finances consciously, the more likely they are to achieve long-term financial success. It’s all about taking that first step, setting clear goals, and committing to making informed decisions regarding finances for young adults.

Embrace your financial journey today, and equip yourself with the knowledge and tools to succeed!