As you venture deeper into your 30s, you may find yourself reflecting on your career, relationships, and, of course, your finances. It’s an important decade for financial planning, as the decisions you make now could set the stage for your future. But how should your finances look by the time you’re 35? This article aims to guide you through the pivotal aspects of planning and managing your finances in your 30s to ensure you are on the right track.

Understanding Finances in Your 30s

Your 30s are a transformative time where personal and professional growth goes hand in hand. Many people begin to prioritize their financial goals, focusing on building a solid foundation for their future. Understanding what a stable financial situation looks like by the time you’re 35 can help you create actionable steps towards achieving it.

Budgeting and Managing Expenses

One of the cornerstones of good financial health is budgeting. If you’ve avoided creating a budget in the past, now is the time to start. Having a clear picture of your income and expenses allows you to manage your finances effectively.

Establishing Your Budget

Start by tracking your income sources and monthly expenses. Consider using budgeting apps or spreadsheets to get organized. Aim for the 50/30/20 rule: allocate 50% of your income to needs, 30% to wants, and 20% to savings and debt repayment. This formula can provide a balanced approach to managing your finances in your 30s.

Saving for Emergencies

A key element of your financial strategy should be an emergency fund. Ideally, you want to set aside three to six months’ worth of living expenses. This cushion will not only help you face unexpected situations, such as job loss or medical emergencies, but it will also give you peace of mind. Remember, building this fund takes time; start with small contributions and gradually increase as you get accustomed to budgeting.

Investing Early: A Game Changer for Your Finances in Your 30s

The earlier you start investing, the more your money has the potential to grow. The power of compounding interest means that even small amounts can add up significantly over time. It’s crucial to educate yourself about different types of investments, from stocks to bonds, and real estate.

Retirement Accounts

If your employer offers a retirement plan, such as a 401(k), take advantage of it. Many companies match contributions up to a certain percentage, which is essentially free money. If you don’t have access to a 401(k), consider opening an Individual Retirement Account (IRA). These retirement accounts can help you maximize your savings and reduce your taxable income.

Consider Diversifying Investments

Diversification is a strategy that involves spreading your investments across various types of assets to reduce risk. This can include a mix of stocks, bonds, mutual funds, and possibly real estate. Investigating your options and seeking advice from financial advisors can set you up for healthy growth as you navigate your finances in your 30s.

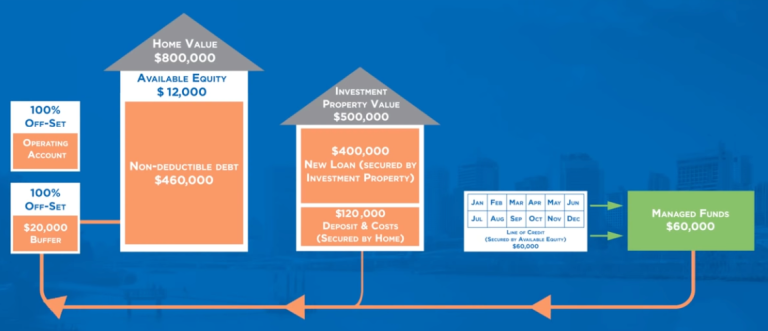

Image: How Your Finances Should Look by 35

This image captures the essence of how to manage your personal finances effectively as you reach the age of 35.

Debt Management for Healthier Finances in Your 30s

As navigating life often brings unexpected expenses, managing debt becomes crucial. Whether it’s student loans, credit card debts, or a mortgage, keeping these in check is part of maintaining a stable financial path.

Creating a Debt Repayment Plan

Analyze all your debts and rank them based on interest rates. Consider using strategies like the snowball or avalanche method for repayment. The snowball method focuses on paying off smaller debts first, which can be motivating, while the avalanche method prioritizes higher interest debts, which can save you more money in the long run.

Limiting New Debt

Being intentional about when and how you incur new debt is just as important as paying down existing debts. Before making any large purchases, ask yourself if the debt is necessary and if it can fit comfortably within your budgeting goals. This is a vital step in ensuring that your finances in your 30s remain robust.

Planning for Major Life Events

Your 30s are often filled with significant life changes, such as marriage, starting a family, or buying a home. Each of these events comes with substantial financial implications.

Homeownership: A Financial Asset

Purchasing a home can be one of the best investments you make. However, it’s essential to educate yourself on the various costs involved, from down payments to closing costs. Consult with real estate professionals and understand your credit score to secure the best mortgage available.

Starting a Family

If you’re considering starting a family, think about how this will impact your finances. From healthcare costs to child care provisions, anticipate any considerable expenses that may arise. Begin saving early, and look into family budgeting techniques to adjust your existing plans.

Final Thoughts on Finances in Your 30s

Reaching 35 is an important milestone, and it’s vital to ensure your finances reflect your aspirations and goals. Throughout your 30s, aim to build a strong financial foundation that can support both present comforts and future needs. Remember to remain adaptable, as life can bring sudden changes. Regularly revisit your financial plans and adjust them accordingly to keep your path aligned with your goals.

With the right planning, savvy budgeting, and informed investment, your 30s can set the stage for a financially sound future. So take the present seriously, invest in yourself, and stay aware of the opportunities around you – after all, the decisions you make today influence the life you’ll lead tomorrow.