In today’s fast-paced world, managing debt can feel like an uphill battle. With the prevalence of easy credit and financial temptations lurking around every corner, it’s no wonder that many find themselves trapped in a cycle of poor borrowing and debt. However, there’s light at the end of the tunnel. By adopting strategic debt management techniques, it’s possible to break free from the shackles of overwhelming financial burdens. In this article, we will explore actionable strategies for those grappling with poor borrowing and how they can reclaim control over their finances.

Understanding Poor Borrowing: An Overview

Before diving into effective debt management strategies, it’s crucial to understand what poor borrowing means. Poor borrowing refers to the practice of taking on debt that is beyond one’s means, often resulting from impulsive purchasing decisions or a lack of financial education. This can manifest through high-interest loans, credit card debt, and other financial obligations that pile up over time. It’s essential to recognize the signs of poor borrowing habits early to avoid a snowball effect that can lead to severe financial distress.

Identifying Underlying Causes of Poor Borrowing

When tackling the issue of poor borrowing, one must first identify the root causes behind these financial choices. Often, factors such as lack of budgeting skills, insufficient financial literacy, or pressure from societal expectations contribute to unhealthy borrowing habits. It’s important to reflect on personal financial behaviors and recognize triggers that lead to impulsive spending.

Formulating a Budget as a Debt Management Strategy

One of the most effective debt management strategies for overcoming poor borrowing is creating a detailed budget. A budget serves as a roadmap for your finances, helping you track income and expenses. Here’s how to formulate a budget that can guide you towards financial stability:

- Assess your total income: Calculate all sources of income, including salary, side gigs, and any passive income streams.

- List all expenses: Document fixed expenses (rent, utilities) and variable expenses (food, entertainment) to identify spending patterns.

- Set spending limits: Allocate a specific amount for each category to control overspending.

By having a clear understanding of your financial situation, you can make informed decisions that directly address poor borrowing behaviors.

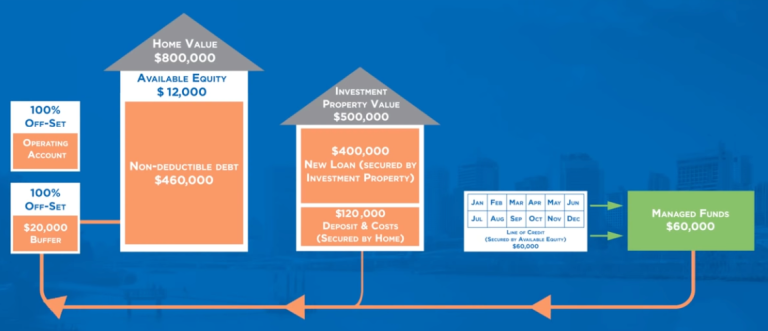

A Practical Image of Debt Management

This image encapsulates key debt management strategies that can help anyone struggling with poor borrowing. From prioritizing high-interest debts to considering debt consolidation options, visual learning can significantly enhance understanding and implementation of these strategies.

The Importance of Emergency Funds in Debt Management

Building an emergency fund is often a neglected yet vital part of debt management strategies. Many individuals facing poor borrowing often lack a financial safety net, causing them to resort to high-interest credit options in times of need. To combat this, aim to save a small percentage of your income each month. Start with a target of $1,000, then gradually work towards covering three to six months’ worth of expenses. This cushion can provide peace of mind, reducing the urge to borrow out of desperation.

Implementing Debt Reduction Techniques

Once you’ve recognized the need for change and established a budget, it’s time to implement specific debt reduction techniques. Understanding and utilizing these strategies can greatly aid in overcoming poor borrowing:

Consolidating Debt

Debt consolidation involves taking out one loan to pay off multiple debts. This not only simplifies your payments but can also lower your interest rate, especially if you have high-interest credit cards. However, it’s crucial to avoid accruing more debt after consolidation; maintaining discipline is key to successful debt management.

Method of Snowball or Avalanche

Many experts recommend using either the snowball or avalanche methods for tackling debt. With the snowball method, focus on paying off the smallest debt first to gain momentum. Conversely, the avalanche method targets the debt with the highest interest rate first. Both strategies encourage timely payments and provide a sense of accomplishment. Choose the method that resonates most with your financial personality, keeping in mind that both require commitment and consistency.

Changing Mindsets: A Key to Overcoming Poor Borrowing

Debt management isn’t solely about numbers and strategies; it’s also a psychological battle. Changing your mindset about borrowing and spending is essential in overcoming poor borrowing habits. Here are ways to cultivate a healthier relationship with money:

- Educate yourself: The more you understand financial concepts, the better equipped you are to make informed decisions. Seek out financial literacy resources, workshops, or even online courses.

- Practice mindfulness in spending: Before making a purchase, ask yourself if it’s a want or a need. This will help curb impulsive buying.

- Set financial goals: Having clear, reachable goals can serve as motivation to stick to your budget and debt repayment plan.

Seeking Professional Help for Debt Management

In some cases, poor borrowing might require outside assistance. Seeking help from a financial advisor or a credit counseling service can provide personalized advice and structured plans to manage debt. These professionals can help you explore options like debt management plans or even negotiate better terms with creditors.

Conclusion: An Ongoing Journey of Debt Management

Ultimately, overcoming poor borrowing and mastering debt management strategies is an ongoing journey. It requires commitment, self-discipline, and a willingness to change financial behaviors. By implementing effective budgeting, exploring debt reduction techniques, and fostering a positive mindset about money, you can navigate through the complexities of personal finance. Remember, achieving financial health is not an overnight process, but with patience and determination, the path to success is well within your reach.